“83(b)” is a tax election that saves startup founders a lot of money. It’s essentially free money for founders. Unfortunately, there’s an arbitrary 30 day deadline, and it’s easy to procrastinate and miss the filing.

If the 83(b) window has closed, there are still a few tricks startup lawyers can use to re-issue the grant and restart the 83(b) clock.

Wait, Remind Me About 83(b)?

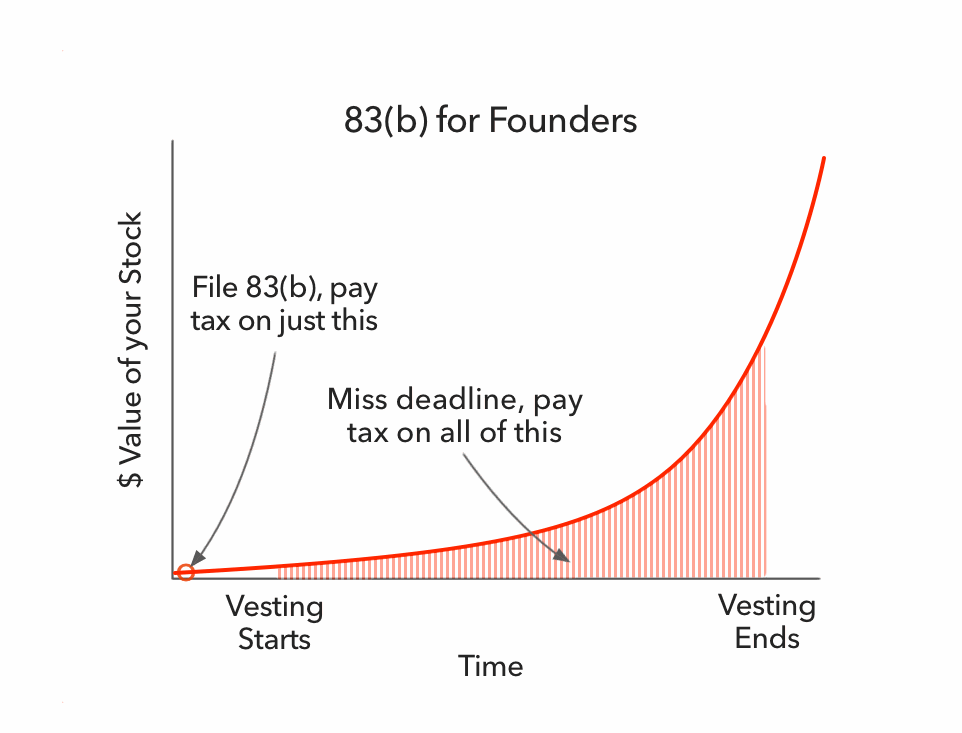

If you just received STOCK from a startup, and that stock is subject to VESTING, then filing an 83(b) election within 30 days will substantially reduce your tax bill.1

Without 83(b), you pay tax on the paper value of your stock as it vests. That’s basically the area under the curve in the figure above. Your stock vesting schedule is probably like “4 years with a 1 year cliff.” If your stock vests during a period of hyper-growth, you will pay hyper-taxes. An 83(b) election fixes this problem.

With an 83(b), you are taxed on the value of the stock on the day you receive the grant. As a founder on day one, your stock is generally worth zero dollars. Your total tax on that will be about zero dollars.2

83(b) TL;DR: file this to pay your tax early when the tax bill is basically $0.00.

See also, What’s my startup’s stock worth?

Salvaging a Missed 83(b) Deadline

Missing an 83(b) deadline is bad. Very bad. Like a tax Chernobyl. However, it’s sometimes possible to call a mulligan, and re-start the 83(b) clock.3

Here are three tactics for salvaging a blown deadline.

1. Cancel the Grant and Re-issue a New Stock Grant

When a startup is still pretty new, it’s probably OK to just cancel the old stock grant, and reissue a new one. For example, let’s say a founder was granted stock on January 1, and it’s now February 1, and they just remembered they were supposed to file an 83(b). The company might cancel the January 1 grant, and reissue a new February 1 grant. The founder would then have a new 30 day clock, starting on February 1, to file her 83(b) election.

This is pretty easy. Just double-check that you’re not generating cap-table drama by cancelling and re-issuing stock. Also, double-check that you are not doing fraud, and don’t confuse this with backdating options. Do NOT backdate stock options.4

If you’re concerned that the IRS would disregard this cancel/re-grant as a sham transaction, you might do the new grant with a different vesting schedule or a different number of shares. I’m not saying that is necessarily enough to pass IRS muster, but the greater the difference between the cancelled grant and the new grant, the safer you are.

2. Adjust the Vesting Language to Repurchase at Fair Market Value

An 83(b) should be filed when you receive stock that is subject to a “Substantial Risk of Forfeiture.” For our purposes, if stock has a vesting schedule, then it is subject to a Substantial Risk of Forfeiture. With a vesting schedule, the forfeiture risk is that the stock owner will quit or get fired, and then the company will buy back the stock. Most, but not all, vesting schedules will be subject stock to a SRF.

Founders generally get a standard “Restricted Stock Purchase Agreement” with a standard-ish vesting schedule. And under this document, the company has the right to buy back the founder’s stock if she doesn’t stick around. Specifically, it can buy back the founder’s stock at the original purchase price (which is generally “par value” - pretty close to $0.00).

But a restricted stock grant doesn’t need to be so stingy with the repurchase price. Instead of repurchasing at the original purpose price, it can repurchase at Fair Market Value (“FMV”).

When the repurchase right is at FMV, then there is no “Substantial Risk of Forfeiture.”5 If there is no SRF, there is no tax-as-stock-vests problem. You would owe taxes right away, when the tax is basically $0.00. There’s no need to file an 83(b) at all under this scenario.

So, after a normal stock grant has been made to a founder, and that founder has missed her 83(b) deadline, the company could agree to amend the stock grant to change the repurchase price from par value to FMV. This solves the 83(b) problem.

However, it does create a bit of a new problem for the company. If the founder leaves during her vesting period, the company may need to shell out real money to buy back the stock, instead of its usual right to repurchase the stock for free(ish).

3. Change the Vesting Schedule to Vest Immediately

A third option is to amend the restricted stock grant to remove the vesting schedule. Without vesting, there is no “substantial risk of forfeiture”, and the stock grant will be taxed right away (when the tax bill is essentially zero).

The obvious downside here is that, without vesting, the founder can now bail on the startup any time and keep her whole stock grant.

But there’s another trick we can pull to minimize this disappearing-founder risk. We can re-apply the vesting schedule later. The thing to note here is that we can’t re-apply vesting right away. Instead, we need to wait until the stock grant is “old and cold”.

How old is “old and cold”? There is no hard and fast rule here. Most tax practitioners consider 6 months to be a safe ballpark, but talk to your tax counsel to confirm. After the “old and cold” period, the newly re-applied vesting schedule will not require another 83(b) election.

Conclusion

Please just file your 83(b) tax election as soon as you receive a restricted stock grant. If you procrastinate, it’s easy to forget. It’s a mistake that can sometimes be fixed, but any of these fixes will run up additional legal bills.

Disclaimer: While this blog is never legal advice, this post is extra not legal advice. And while I’m a startup lawyer that regularly advises clients on tax-related formation issues, I’m really not a tax expert.

-

Probably! but consult with your tax advisor to confirm. ↩

-

Founder stock is generally worth zero dollars at the outset, unless there are some unique circumstances giving your company a higher valuation at formation. ↩

-

“Homer, your bravery and quick thinking have turned a potential Chernobyl into a mere Three-Mile Island.” ↩

-

Ben Horowitz on not backdating stock options: Why I Did Not Go To Jail. ↩

-

Why? Maybe the IRS thinks you’re not “forfeiting” anything if you’re being paid the fair market price for it. See Treas. Reg. § 1.83-3(c). ↩